Inside the Pod: Episode 7

In our ongoing profiles of wealth management firms combining human expertise, empathy and guidance with technology, data and tools, I recently had the pleasure of interviewing Rachel Schnoll, Managing Director of FinLife at Goldman Sachs Personal Financial Management (the rebranded United Capital entity).

They represent many areas of our business I'm passionate about from the art and science they bring to delivering a client experience built around helping clients "live richly", to the flexible advicetech platform they've invested in to help free up and empower their advisors to work with clients, as well as how, while they started out as a traditional RIA, they "TAMP-ified" themselves so they could offer FinLife to independent RIAs (of which Rachel shared with me they now work with more than 50, including 18 new firms year-to-date).

Rachel shared updates on how Goldman Sachs is integrating United Capital and FinLifeCX into the business, creating synergies both for other parts of Goldman and referrals to PFM.

Press play to learn what’s attracting advisors and helping them attract, engage and retain clients.

Show Notes

· One year after the acquisition of United Capital, how GS rebranded and integrated the business including FinLife CX [2:00]

· The FinLife client experience platform [5:45]

· How FinLife became a TAMP platform offering to independent advisors [7:08]

· Profile of the FinLife TAMP advisor [9:15]

· Breaking down the FinLife toolset and prescriptive process [11:38]

· The client experience and reaction [16:00]

· The importance of engaging both partners/spouses in the process [24:09]

· FinLife Investment Viewfinder – making tradeoff decisions [25:42]

· How the FinLife tools helped advisors and clients in March [28:25]

· Leveraging a prescribed process for the entire client journey [29:54]

· Empowering clients to live richly by giving them permission [32:56]

· Aligning pricing to the value of life planning [34:42]

· PFM as part of the broader Goldman Sachs client segmentation [37:49]

· What’s next for PFM and FinLife [40:55]

Podcast Transcript

Wealth Management v2.0: The AdviceTech Revolution, Episode 7

with Rachel Schnoll, Managing Director, Goldman Sachs Personal Financial Management, FinLife Partners

Gavin Spitzner (President, Wealth Consulting Partners, LLC):

Welcome to the "Wealth Management Version 2.0, the AdviceTech Revolution" podcast, where I'm joined by Rachel Schnoll, Managing Director of Goldman Sachs who took the reins of the FinLife CX Toolset and RIA solution that came along with Goldman Sachs’ 2019 acquisition of the $25 billion RIA, United Capital.

On this podcast, we're focused on the business of the business, the business of advice, and specifically, we study and celebrate firms that are leveraging the combination of technology and humanity to deliver better advice to more people, and better outcomes for more people through that combination. I call that the “AdviceTech Revolution”. And Rachel, and the Goldman Sachs PFM team and the FinLife CX team, they're on the front lines of that revolution. And they combine many of the traits that I think are so important to be successful in this business. They started off with strong RIA DNA, built up capabilities that service them and, over time, saw that that was something that they could leverage for other advisors as well.

They did the hard work of the tech integration, figuring how to leverage data effectively, building workflows to support consistent, excellent client experiences. And Rachel, you've got a value proposition that I absolutely love in terms of living life richly. There's so much doom and gloom in this business, a lot of marketing to fear, outliving money, and we'll get into that.

So, Rachel, I won't ask you to go all the way back to the United Capital origin story. We'll save that for Joe Duran for another time. But it's been just over a year since Goldman Sachs acquired United Capital. Give us some background on that and how the integration is going.

Rachel Schnoll (Managing Director Goldman Sachs Personal Financial Management, FinLife Partners)

Well, Gavin, first of all, thank you so much for having me. This is a great podcast and really important to what's going on in wealth management right now. I appreciate the time and effort that you put into this. With regard to the United Capital acquisition, as you mentioned we closed in July of 2019. So, it's been, we're sitting here in August now so it's been just a little bit more than a year since we closed and the last year has really been about integrating PFM into Goldman Sachs and keeping what's amazing about PFM, which is really putting the client experience first, and caring about what matters to individuals and building their life plan around that. And as you mentioned, helping clients live richly instead of just dying rich, which is, you know, historically what our industry has done. We're all about getting to retirement and making sure you don't run out of money in retirement, but sometimes, maybe forgetting about how we're living along the way.

That's the framework that Joe Duran set up and it's still the North Star of United Capital. So, the first order of business was we rebranded…what was United Capital is now Goldman Sachs Personal Financial Management, or Goldman Sachs PFM. And we've also been trying to bring a lot of the benefits of being part of a larger organization to the clients of PFM. So, this has manifested itself in some new investment strategies on the platform, a new asset allocation regime. We're bringing the asset allocation and also the third-party product selection that's used in the Goldman Sachs Private Wealth Management business, which really focuses on clients with $10 million and above and really much larger than that. We brought that all to PFM. So, all the asset allocation is done by the same team as is done through Goldman Sachs Private Wealth Management, and we're also bringing that to FinLife partners. So, whether you are a client of the PFM advisor or you're a FinLife partner, you have access to that same wealth management platform.

Another thing that we've really done is sharpen the technology. As many entrepreneurial organizations know, what was really crucial to United Capital was getting out new technology quickly and making changes to the platform. And I think Goldman's put a little bit more of a process around that. So, we're not getting things out maybe as quickly as they did in the past at United Capital, but there's a little more rigor to the introduction. So, it will be in a more mature state when the new technology is released…that's what we've seen…really focused on the integrations, keeping what's great about United Capital, now Goldman Sachs Personal Financial Management, but then bringing some of the best of Goldman Sachs to the PFM client base.

Gavin: Fantastic. And we'll get more into that. But let's take a step back. When you talk about FinLife partners, talk to us about that…give us kind of the baseline. What does that look like as an unaffiliated advisor or advisory firm? What comes with that? What are my options? What's the flexibility? Can you give us a little overview?

Rachel: Well, first, let me just give a little background about what FinLife is. FinLife is a client experience platform that was developed by United Capital for the use of United Capital advisors, now PFM advisors. So, United Capital was built through acquisition. And every single office that was added had a little bit of a different way of interacting with advisors. So, what FinLife brought was a unified client experience for all the United Capital clients. And it really consists of three behavioral finance exercises that we take the clients through that are very interactive, that are really about how they relate to money. And then a number of digital tools for both the client and the advisor that really helps the advisor manage their clients. And so, that was introduced to United Capital.

And then as United Capital was speaking to other firms about acquisitions, sometimes the acquisitions didn't work out for one reason or another. But those advisors that wanted to stay independent were still really interested in the FinLife platform.

And so, about four years ago, we started to offer the FinLife platform and make it available to independent financial advisors. And so, you can retain your independence and still use the FinLife client experience platform. We've made it really easy for an independent advisor to use. For example, you keep your tech stack. So, whatever CRM you're using, the planning software that you're using, the portfolio accounting, or portfolio management system that you're using, we will connect FinLife to those different systems via API integrations. We know that the reason why advisors want to remain independent is because they want choice. And we want to support that ability to have choice. Another way that we kind of celebrate that choice is that as an independent advisor, you can interact with the FinLife toolset in many different ways. You can just purchase the technology from us or you can use our investment management platform if you want to outsource investments, you can outsource insurance or risk management to PFM.

We have some banking services that we can offer, we can introduce you to Goldman Sachs investment strategies so you can have access to that, or you can just interact with us on the technology side. So, whatever works for your business, we're happy to work with you in that way.

Gavin: I don't know if you can generalize, but is there a general profile of an advisor, frankly, an unaffiliated advisor, choosing to work with you, or somebody that partners up more formally, in terms of the way that they run their practices…you talk about the behavioral finance aspect of some of the tools and the digital engagement. So, I'm guessing that it may not appeal to a hardcore, "My value proposition is asset management as much as something that's more focused on planning and client engagement."

Rachel: Yeah, so usually, when I get asked that question people want to know about the AUM, right? So, what's the AUM profile of your clients, and really, we have clients from just under $100 million to multi-billion dollar. So, the AUM is really less important than the mindset of the advisor and how they're running their business. And so, Gavin, you hit the nail on the head. We generally work with advisors that have a planning mindset and really want to move their practice from just conventional planning to conventional financial planning to life planning, because we're going to give you the tools to do that.

And then also the advisor has to have a growth mindset. What doesn't generally work for us is the advisor that's running $200 million in assets. It's one or two advisors and they're good, right? We want advisors that might be one or two advisors managing $200 million but are looking to grow, are looking to get to $500 million. And what we've seen with FinLife is that it gives them the ability to scale their business, to bring on additional advisors and get to that next level of AUM that they're hoping to achieve.

Gavin: Right. So, talk about that. Actually, I looked at some of the case studies on your site, and the common thread, I'd say across all them was not only their growth in assets and revenue but a strong focus around profitability. So, can you talk a little bit about that? Where are they gaining efficiencies in terms of their spending? How's it kind of creating that flywheel effect where they can really scale up the practice?

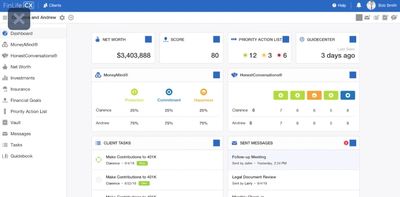

Rachel: Yep. So, what FinLife allows you to do is really three things. So, number one, those behavioral finance tools that I mentioned help you get to know your clients better. The second thing that it does is it helps you go digital. And we give you an app that your client can put on their phone, and you can interact with your client via that app. Something called AdvisorCenter, which becomes your sort of center of truth in terms of managing your clients that connects to the rest of your tech stack. And then by giving you those tools, it helps you give scale to actually grow your business. And so, what we find is that many, I mean, most independent advisory firms were started by one person or two people, and they have a certain way of doing business. But as they're looking to pass that business on to the next generation, or as they're looking to bring on additional advisors, what they have been doing might not translate to the next person. So, Gavin, if you and I are working together, and you established the business, you know, the way you interact with a client isn't necessarily the way I interact with a client.

And then you have to have a meeting of minds like, okay, are we going to act differently or independently? What about when we bring on, you know, Marilyn, who's going to be our third advisor? How is she going to interact? And so, what we really see, the scale happening with FinLife is it gives everyone in the office the same way of interacting with the clients, which just saves so much time, right? Like, we would talk to one of our clients, we used to spend a lot of time putting together an agenda for the meeting. Now, the agenda is the list of items that they discussed at the last meeting that are on the PAL, that's our Priority Action List. So, you know, that's just one small example. But really having everyone in the office conducting meetings in the same way gives you that scale to really grow your business, and then the opportunity to outsource different facets of your business if you choose to do so can also give you that scale. You know, not having to do the trading, for example, if you're outsourcing the item and not having to do the research on the investments as well.

You know, that's another time savings that can drop to the bottom line when you're spending more time with clients. And one of the key things that we do to help provide that scale is we do a lot of training. So, when a new RIA becomes a new FinLife partner, we do something called Bootcamp. And in previous times, we would bring them into Dallas for three days where we do an intense training, and that helps them understand how to use the FinLife tools. We will tell you, with a new prospect, meeting one, you do this, meeting two, you do that, meeting three, you do this. It's a very prescriptive practice management tool that allows you to get the scale in your business. So, you don't have one advisor in your office doing five meetings before they close a prospect and someone else doing, you know, six meetings. It's, "This is how it's done, this is the information that you're getting, here's the, we'll give you the tools to give a guidebook, and the investment proposal to your client." It's all very prescribed and so you don't have to be spending time thinking about that.

Gavin: My clients are out there watching this, are smiling seeing me smile because the whole notion of being prescriptive is something I talked to my advisory clients about a lot. And, you know, that it takes two to tango, you need advisors that are open to that, recognize there is a better way to do it. And to scale and to have consistency, you kind of have to do that but what you're prescribing has to be effective and able for...advisors need to be able to deliver with that training and that practice management support effectively.

Why don't we turn that around a little bit from a…I'm interested from a client point of view.

I get it from the advisor perspective, the efficiency, the prescriptive process. I'm guessing there's a lot around the data, and how that flows into different parts of that process, and I'll come to that. But from a client point of view, what have you seen? What does that experience look like? What are the some of the digital tools that you're putting in front of them to help them get engaged and stay engaged?

Rachel: So, what we see a lot, and I'm sure you've seen this with your clients and folks who are listening, see this, is that you get, in a typical relationship, it might be a married couple. And there's one half of the married couple that's very engaged with the financial advisor and one that's less engaged. And the reason is that one person cares a little bit more about finances and money and one person is less engaged with money. And so, we have three behavioral finance tools. They are about how you interact with money, not in behaviors, and not around the specifics or the technicalities. So, we're never going to bring up, "What's your risk profile," right? In one of the first three meetings. But rather we're going...the very first interaction that we do when you're a FinLife client is something called the MoneyMind. And this is something that an advisor would send to a prospect and, or a new client. And it's a series of seven questions. And these seven questions are, it's multiple choice, it's all digital.

And the questions are, "A Girl Scout is selling cookies outside of the supermarket. What do you do? You walk by, you buy 10 boxes, or you buy one or two to be a good, you know, citizen?" And what that does is measure your quick brain reaction to money. And if you were to buy, and at the end of these seven questions, every person is ranked amongst three different attributes. So, one is happiness, the Happiness MoneyMind, the Commitment MoneyMind, and the Protection MoneyMind. And Protection MoneyMind really means that you are concerned about spending money and you may have $10 million, but it's never going to be enough. You're always concerned that you're not going to have enough money. The Commitment MoneyMind means that you'll spend money, but you're spending money to support other people. And then the Happiness MoneyMind is someone that spends money perhaps frivolously to, you know, engender their own happiness and, you know, wishes.

And what we generally find is people are a combination of all three, but that's so helpful to people to understand how their quick brain reacts to money, and you'll see many, you know, married couples who'll say, "Oh, my gosh, I totally knew that you were Protection," or, you know, and sometimes that causes a lot of friction in a relationship if you have a Protection MoneyMind and a Happiness MoneyMind. And so, it really opens people's eyes to see why they might be fighting about money. Because the Protection MoneyMind is always saying, "Oh, my gosh, we can't spend anything, we don't have enough." And the Happiness MoneyMind is saying, "Oh, let's go on that vacation, let's stay at the fancier hotel, you know, we deserve it." And that can cause friction within a relationship. So, that's the first step and it's so helpful to the advisor also, because the advisor then knows how, you know, what direction they might have to take this relationship, right? So if you've got Protection MoneyMinds, they might be over-saving and denying themselves things that they can actually do.

So, it's then up to the advisor to redirect them and say, "Well, you've always wanted this lake house, you know, you guys can afford it and you're still going to be okay." Or the Commitment MoneyMind, like that sounds really great. Like, "Oh, I don't spend money on myself, but I spend it on others." But that can be dangerous, right? If there's a parent that's constantly giving money to a grown child and not saving for their own retirement. So, these are things that are important for an advisor to understand and also for clients to understand about themselves. So, first step is the MoneyMind. The second step is something called Honest Conversations. And this is really the crown jewel of FinLife. So, Honest Conversations is when the prospects or the clients come into the office, or we can do it remotely, all digital. So, that's actually been a great help in recent times is that all these steps can be done either in person or remotely and with digital tools. So, Honest Conversations is where you sit down with the advisor and you can, if you're doing it in the office, physically, we have cards and there's 15 cards.

And the cards ask how, this is the slow brain thinking. What's important to you? What kind of values or things are you trying to achieve in your life? Is it things like, "I want to spend more time with people I care about," "I want to leave a lasting legacy," "I want to educate, you know, my children." And so, both people in a relationship who are your clients would then rank the things that are important to them. And then they have to come together and rank the top five things that are important to them as a couple. And so, what's so critical about this exercise is it engages both people in a relationship with that financial advisor. And again, it's not about money. We're not talking about the beta of your portfolio or whether you want to go into large-cap growth or large-cap value, or what stock you like, or how much stocks versus bonds you're going to have. We're talking about what you as a couple want to achieve with your life. And the money is just the fuel to achieve those objectives. And so, in these conversations, you know, we hear time and time again that people cry, that spouses find out things about each other that they never knew were important to their spouse.

I've heard of two Honest Conversations that resulted in the couple moving homes. One of those conversations actually happened with a guy who's on our FinLife team. And he and his wife did Honest Conversations with a PFM advisor, and he said, "Bring your check-," after he did it, he tells everyone, "Bring your checkbook to Honest Conversations," because he found out that his wife hated their house and they wanted to move and they did. So, he had kinds of things...

Gavin: Through inertia, people, they don't know the possibilities, they don't know what each other's thinking. When you look at the stats around what happens after death of a spouse, a divorce, and people leaving their incumbent advisor, off the charts, that ability to have those tools and have that framework to bring people together, that alone is just so, so important. And many advisors just, they, you know, they're trying to bring on a new client, if they're dealing with one person and that person can execute, they're comfortable just moving ahead with that, and it's very short-sighted.

Rachel: Yeah, and not only that, Gavin, so you're absolutely spot-on, right? Engaging with both spouses helps you keep that relationship after what we call the CFO spouse, you know, if something happens. If there's a divorce or if there's a death in the family. So, not only does it keep that relationship with the advisor, but also now you're getting referrals from not just the one spouse but from both spouses. And generally, the less financially engaged spouse, even if they went to meet the advisor, you know, they're looking up at the ceiling and not really paying attention. But the non-CFO spouse feels so engaged by this conversation that they go out and you get more referrals actually from the non-CFO spouse than you do from the CFO spouse, because they've never had an experience like this before. And that goes back to your earlier question about growing revenue, right? Now you've doubled your referral sources from, you know, your clients because you're engaging with both spouses. And so, that helps you grow your client base, and your revenue.

Gavin: I think that was the second of three. Was there a...

Rachel: Oh, right. So, the third exercise is about, it's called Investment Viewfinder. And Investment Viewfinder is a great conversation for the advisor to have with their client to kind of explain the trade-offs that you make in investing. And again, in a very simple way. So, the four attributes that are in Investment Viewfinder are performance, protection, taxes, and expenses. And if you were to ask someone, "Well, what do you want? Do you want a high-performing, low-risk, inexpensive, and, you know, low-tax portfolio, which is the most or what do you want?" They would say, "All of it," right? But you can't have all of it. Investing is actually a series of trade-offs. So, what Investment Viewfinder does is it gives an advisor digital tools, and we actually have a slider bar. So, the advisor can then have the conversation with the client about performance or risk, which is more important to you? And you can see that on the slider bar, which trade-offs you're making, and then for each, we show each attribute next to each other. And the advisor can walk through with the client, you know, where they want to make the trade-offs in a portfolio.

And the advisor can also, for example, if it's an advisor that believes in index products or an advisor that believes in active, that might be more, have a slightly higher cost. The advisor then gives them the ability to explain the trade-offs that the client is making and why the advisor believes that those are in the best interest of the client. So, it's a really great way to slowly bring in the investment conversation, but still in a very understandable way that, again, is not jumping right into risk or beta or any of those more technical terms.

Gavin: Right because of the foundation you set with Honest Conversations and all that's come before, by the time you get to the investment side, that's not what you're selling, that's just the way to achieve what you've already laid out.

Rachel: Yeah, you're 100% right. And that's why we say money is just the fuel, right? And that's why you hire an advisor, right? You're hiring an advisor to, one, I think the number one thing that people want to hear from their advisor is, "I'm okay," right? "Just tell me I'm okay." And that is what we hear from the FinLife advisors is that in March when stocks were really volatile, the FinLife tools allowed them to change the conversation with their clients, so that in other market downturns, they might have had to talk about, "Why is my portfolio down 20%?" But now because we give you a score, we pull in the score from your financial planning that says, you know, you're 80%, you know, you've got an 80% chance of achieving your goals in retirement. The advisor can say, "Market's down 20% but you're still in the green zone, you're okay. And you can still buy the lake house and you can still pay for your child's education, and you're okay." Or they can say, "This market downturn really affected our score, let's figure out what we need to do to address that…You need to start saving more…maybe we need to adjust your portfolio," but it gives very helpful tools to be able to change the conversation away from “my portfolio underperformed the S&P 500” to, "Can I do the things that I want to do?" and, "Am I on track?"

Gavin: I love the focus on the art and the science. And the fact you've got a very regimented process to get somebody to the onboarding stage, you're not leaving it to chance. I'm a big fan of that, to be able to set out with a prospect, "This is our process, this is what it's going to look like. We're going to have two meetings, three meetings, whatever it is. Make sure we're aligned, we understand what the money's for, all of that." So, you're not later in the relationship trying to back into all that stuff when it's much harder. I'm guessing just like you have that very prescribed process upfront that you have the same thing in terms of onboarding and then ongoing client experience management. Can you talk about, then what is the experience of a client?

Rachel: So, after you've taken the client through the three behavioral finance exercises, you're going to create a PAL, a Priority Action List for the things that you want to achieve for your clients. We need to get your life insurance set up, we need to set up a college education fund. And then you're going to create tasks around those PAL items. And then you're going to send those tasks from the AdvisorCenter over to the client through GuideCenter, which is the app that's on their phone, and they'll see... So, I'm your client, Gavin, and I see, I've got to schedule the appointment with the doctor for my new life insurance policy, right? And then you can tell the advisor when you've done that and send it back and they know. Or the advisor can remind you of some of the things that I talked about moving from just conventional financial planning to life planning. I mean, some of the action items might be things like, you want to spend more time on, so going back to the Honest Conversations.

The number one Honest Conversations card that we see from clients is "spend more time with those I care about." So, how do you do that? There are many folks that are older, that have grown children. And one way we see advisors helping their clients is, helping their clients execute on "spend more time with people I care about" is plan a family vacation. You can say, "You've got the money, you've saved this money, what are you going to use it for?" Plan a family vacation, take the whole family and then that becomes the task. The task becomes, "Did you talk to the travel agent or did you make the hotel reservation," or, you know, and that is another way that financial advisors may not think that they're adding value, but they're actually adding tremendous value. And that's so meaningful and important to that person, they're clients for life. And they're going to recommend that their children meet with you as well.

Gavin: Yeah. And their friends and their relatives. Advisors that, and here we're talking about wealthier people that have options, right? That, to me, is what wealth is, in that you have options. But there's an awful lot that I'm sure we both know, older wealthy people that, based on their upbringing, whatever it is, they don't give themselves permission to spend and they, back to where we were before, they die really rich. And either they didn't even realize or nobody gave them permission and helped them actually come up with an action plan to spend on the stuff that matters to them. Advisors that give clients permission, and actually help them take action around those things, they're, I mean, they're set. They're no longer in a game of, "Well, yeah, how did you do against the benchmarks last quarter?"

Rachel: Yeah, we have one FinLife partner, they're based in New York City. And they had a client whose grandson loved to play tennis. And this client was one of those people that you just described, you know, grew up in a generation where they were never comfortable spending money, but was worth tens of millions of dollars. And what the advisor got them to do was build a tennis court at their house so their grandson could come and play tennis, which, of course, that makes...I'm getting teared up thinking about that, actually. I mean, how wonderful to spend money in a way that makes your grandson want to come over more and be at your house? And that client would have never given themselves permission to do that without the advisor helping them and the advisor would have never understood that that was important to their client without the Honest Conversations.

Gavin:

All right. So Rachel, I'm curious, with the focus around life planning versus just a pure focus on investment management, is that having any implications for how advisors are charging further value?

Rachel:

Yeah, absolutely. We've seen advisors change their ADV’s and actually we've seen advisors increase their fees and some of our FinLife partners have increased their fees from, say 100 basis points, to 125 basis points for that explicit guidance that they're giving their clients. And, and that's been a big new revenue source. So, , and, uh, so one of our clients did that. They increased the fees by 25 basis points and they only lost one client.

Gavin:

Yeah, I think the whole…the fear of…feeling the need to discount fees, it's in the minds of most advisors that aren't comfortable with the value that they're providing, but with the fee compression we're seeing on the asset management side…providing that incremental service is really the only way to maintain fees. And maybe to your point, grow fees by having more explicit services that advisors are providing.

Rachel:

Advisers need to have confidence in the value that they're providing. And a good advisor that's providing a great client experience and caring about the life of their client and helping them achieve their goals and live richly as I talk about, will absolutely not feel pressure on that fee, because you’re providing value.

Gavin:

Yeah. Clients, if like you say it, if clients feel like they're okay, that the advisor is in some way responsible for that feeling, because they're helping them figure out what they can do, what matters to them, applying their wealth to those things, that's, I won't say that's priceless, but it it' worth more than certainly 75, 80 basis points, which is the average, like for a million dollar client is somewhere in that range. Now, if you're doing all those things, you're giving them permission, you're helping them live the life that they want to live, that's certainly worth 20, 30, 40, 50 basis points, or some kind of an annual fee.

Because you're putting yourself into the realm of a true professional at that point. And it's the old anecdote of when you're with your doctor, you're not negotiating fees. If they're taking care of you, the value is beyond, “oh, I'm going to try to negotiate you down a few hundred dollars.”

Rachel:

That's exactly right. We talk in our training about helping advisors practice at the top of their license and we give them the tools to do that and say you should charge for that.

Gavin:

No doubt. Let’s take it up from a Goldman perspective. Goldman synonymous with exclusivity, wealthy that we just talked about. With PFM, you're serving, I guess, what I'll call mass affluent or lower-high net worth clients as well. Can you speak about what the implications are for that? And being able to serve a more diverse clientele, a broader clientele. And maybe as part of that, you know, how do you think within your area around diversity, being more inclusive and being able to help more people achieve whatever outcomes are most important to them?

Rachel: Yeah, so just as Goldman Sachs has helped the ultra-wealthy people achieve their goals and financial goals, now we're just able to do that with a wider swath of people. You know, Goldman Sachs has historically built many things organically. And as Goldman was looking at, "How do I serve a broader client base?" I think they felt like it was going to be very difficult to build that organically. And United Capital has just been, and now Goldman Sachs PFM, is a great fit for being able to serve that next level of wealth. So, it's been a great fit. And Goldman Sachs is absolutely committed to serving this tier of wealth, which is really the vast majority of people in this country. So, they're limited in the segment. If you're only focused on ultra-high net worth, it was limiting, which is why we chose to broaden out.

Gavin: And I saw some stats that your team had shared maybe a month or two ago that the referral sources from Ayco in the private wealth team into PFM have been really impressive already. I think I saw over a billion dollars of referrals where you couldn't before have served those clients.

Rachel: Correct. I don't know about the number to confirm or deny that number. But there are a lot of referrals that are coming from Private Wealth Management and also our Ayco business, which is a business that's focused on corporations. And what we were hearing…so the Ayco business goes into a corporation and offers financial planning and executive counseling for the C-suite executives. And in many cases, companies want to offer financial planning to a broader swath of their employees. And the Ayco business wasn't built to…they just didn't have the people to be able to serve an entire company…and so, now with PFM, we're able to serve and help more people in those companies achieve their financial goals.

Gavin: Absolutely. So, let's look ahead. As you think about your mission, your value proposition, the clients you serve, the advisors that you serve, what's, how do you look at all that? And how is that influencing your roadmap and where you go next?

Rachel: So, both with PFM and with FinLife, we're looking to grow. So, right now, FinLife services about 9,000 individual clients at all the different RIA firms. And if, as we continue to grow, we can continue to add more features on the FinLife platform and continue to develop the practice management that we offer to advisors. So, being a FinLife partner, I think, has a lot of advantages for an independent advisor because you retain your independence, but you get the client experience, the practice management, the client management, the investment management, should you choose to use it, from Goldman Sachs. So, you get sort of all the resources of Goldman Sachs but retain your independence. And so, we're looking to continue to grow the FinLife platform. And then on the PFM side, continuing to grow the client base there. And I think you'll see a lot more organic growth coming from the traditional PFM business than you saw from United Capital, which was really..the growth was driven through acquisition.

So, I'll just close with, maybe one thing I mentioned earlier, which is that the real crown jewel that Goldman Sachs saw in PFM is the client experience. And it's really unlike..I've been working with financial advisors for over 20 years... and it's unlike anything I've seen anywhere else. You know, to really engage both financial spouses, to change the conversation away from investments and let people know that they're really okay. I mean, that's how you provide value as an advisor. And it's been a real privilege to work with the platform and to work with our partners who are really helping their clients change their lives for the better and live richly.

Gavin: Absolutely. Well, Rachel, thank you so much for the time. It's exciting, it's early days still as part of Goldman. So, we'll be keeping our eyes on what comes. I definitely applaud the focus around client experience and the art form of that and leveraging the technology, the data, and just shifting that focus around how advisors are engaging clients.

I'm a big fan of that and I think that the future of this business is life planning, having that strong technology...it's interesting the way that you've given that flexibility, and the modularity around how advisors want to power some of this while still maintaining that focus around your very unique client experience engagement model. So, exciting… we'll keep an eye on things. And again, thank you so much for the time, Rachel.

Rachel: Thanks so much for having me, Gavin. This was a great conversation.

END